Why Cash on Cash Return Drives My Investing Decisions

- Apr 6

- 2 min read

When I underwrite a deal, I can generate pages of metrics. IRR. Equity multiples. Sensitivity tables. All useful in the right context. But the number I care most about is much simpler.

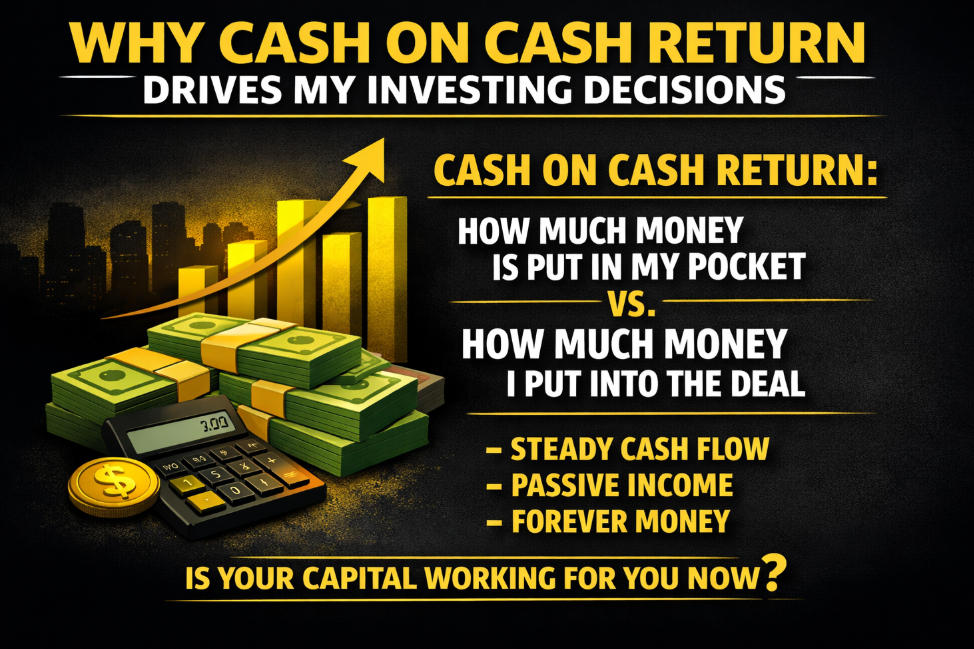

Cash on cash return.

At its core, cash on cash answers a very practical question: how many dollars per year does this investment put in my pocket compared to how many dollars I put into it? That is it. Real cash, relative to real capital.

Many syndicators highlight IRR, which factors in the projected upside of selling the asset years down the road. That emphasizes the “one time money” of a sale. That can be a helpful modeling tool, but it assumes a future exit that may or may not happen on schedule. Because my strategy is long-term buy and hold, I am less concerned with a hypothetical sale and more focused on what the asset is doing for me now.

Cash flow is what supports the portfolio. It funds reserves. It gives optionality. It creates stability. It has created the floor of income on which I’ve built how I fund my life- the “FOREVER MONEY”.

That said, I am not chasing perfection on day one. I am willing to accept a smaller but positive cash on cash return at acquisition if the fundamentals and business plan are strong. My goal is to manage the asset intentionally, increase income, control expenses, and drive performance so that by year two I am ideally seeing double-digit cash on cash returns.

That progression is where strategy meets execution.

For me, underwriting is not about predicting a perfect future. It is about buying assets I can get into while mitigating downside- then actively improve, measure, and manage toward meaningful cash performance.

So when you evaluate your next investment, are you getting excited about projections… or are you focused on how effectively your capital is working for you right now?

Comments